We have covered the two major stories about the development of money, global trade and finance: collectibles and debt. It's now time to look in greater detail at money as it actually works in the modern economy. And it's really difficult to do this, because any classical economics textbook - even from the 1960's - is already outdated.

The best resource we know, which is able to take both a long, historical perspective, but then ground it in the day-to-day realities of money and banking as they actually work in our era, is this course from Perry Mehrling and the Institute for New Economic Thinking. Some videos initially included in Kernel are no longer public, but you can find most of the MOOC if you look through the new playlists on the INET youtube channel linked above.

This course was found thanks to Ethan Buchman, co-founder of both Cosmos and Cycles. cycles.money is based on the realisation - partly implicit in Mehrling's course, that what really drives the action (and hence the power) in the banking system is the liabilities side of the balance sheet, not the assets. Banks have - for a long time - participated in clearing houses, from which most people are excluded, and through which they settle enormous amounts of debt with very small amounts of actual money. We invite you to consider this little-known and wonderfully powerful inversion as you wander through the history of modern banking. The best place to start is this video.

You cannot ask better questions unless you understand something deeply. You cannot understand how to disrupt banks and the current financial system unless you know how we got here and what it actually is.

This series grounds value, money, speech, and incentives in very real-world, practical terms. Literally the entire course is aimed at teaching you how to read the Financial Times and translate it into everyday language for your friends.

While not a core learning objective for Kernel, Mehrling approaches money and banking through the issue of liquidity, rather than solvency, and this is particularly relevant for anyone working on DeFi.

"The analytical apparatus of this course is largely balance sheets."

"The two key ideas in this course are thinking of banking as a clearing system - a payment system - and banking as market making. Additionally, banking as advanced clearing is how we bring in finance and forwards and futures and swaps and derivatives etc."

If you watch the whole course, you'll see Mehrling use the classic T account over and over again to explain increasingly complex concepts. You'll realise that the T account, or balance sheet-style thinking, is just the banker's way of being able to hold in mind complementary opposites and demand, very practically, that they balance each other out. It is a powerful, and simple, way of understanding the flow of value anywhere in the world.

Prompt: T-accounts and thinking in terms of balance sheets are just the way bankers navigate the play of what foundational Kernel pattern?

Complementary opposites.

Banks and shadows¶

Mehrling starts by describing a simple bank: with loans, securities and cash as its assets; and deposits, "other borrowing", and a balancing item of "net worth" as its liabilities. If this seems familiar and boring, stay with it, because this course is really about that strange term "other borrowing", how it relates to the money markets, overnight lending, FedWire and shadow banks - all the stuff you were never taught about because they didn't exist in the form they now take, especially post-2008.

Moreover, instead of focusing on a positive "Net Worth" - i.e. the solvency of banks - Mehrling is going to be looking at that Tamil word for Chinese money: cash and the liquidity problem, because this is actually the constraint bankers have to face at the end of every day when they "clear" their accounts. In many ways Mehrling's course is about payment systems and how they work in practice, and this is why it's so relevant in the context of peer-to-peer electronic payment systems, or open protocols for money. In particular, understanding the current system of shadow banks will enable us to appreciate more specific ways in which it can be improved and what the potential impact of programmable money might be for how responsive the very structure of the system might become.

"We're also going to be talking about shadow banks, [by which I mean] an entity that is holding Residential Mortgage-Backed Securities (loans that have been turned into a kind of bond), or Interest Rate Swaps and Credit Default Swaps to mitigate risk so that what is left is a short-term, relatively low risk asset that can be used as collateral for borrowing in the wholesale money market [...] So, you have money market borrowing as the liability. They're not borrowing from you and me, but from money market mutual funds and big corporate investors. The instruments they're using are things like Repurchase Agreements, Eurodollars (or LIBOR, or SOFR), and Asset-Backed Commercial Paper. The point is: this model is now the dominant one. The amount of credit in the US that runs through this method is much larger than through traditional banks, which is what the textbooks are all about."

Shadow banking also faces the issues of solvency and liquidity, but it's more complex than in the regular system because the issue of liquidity is really about being able to roll over the funding for your RMBS, IRS and CDS. If the money markets freeze up, you can't roll it over and you have to liquidate. This is what a lot of the 2008 financial crisis was about.

Prompt: What are the two key concepts we must understand to program useful kinds of money and create a functional global system with no owners?

Liquidity and the price of money.

The course looks in great detail at the Federal Reserve, which is also a bank. Mehrling begins by discussing a 2012 Fed balance sheet and, for instance, the $852 Billion of mortgage backed securities it was carrying then. Very pertinently, Mehrling shows how

"It's just not correct to say that the Fed is 'printing money'. When it is expanding the money supply, it is expanding both sides of the balance sheet. It is a classic banking operation, which happens at all levels of the system."

Whether you agree that it should happen is another story, but Mehrling takes great care to place himself in an esteemed intellectual tradition which may make you rethink your position. In any case:

"The system has changed dramatically. When people talk about Quantitative Easing 1, QE 2, QE 3 - they're talking about the transformation of the Fed's balance sheet that I am showing you."

The 4 prices of money¶

The difference between liquidity and solvency is important. To be solvent means to possess assets in excess of liabilities, so solvency is really the ability to pay your debts. However, not all assets are “liquid”, which means that you can’t necessarily use them immediately, right this second, to pay a debt if it comes due. For instance, a house is an asset, but you can’t use it to pay for your cell phone bill, without going through a number of intervening steps. Liquidity really means “cash”: all of the value you possess which can be used to pay for debts right now. By law, banks must be solvent, hence the focus of traditional economics. However, Mehrling is making the point here that “liquidity is what really drives all the action” in FedWire, the overnight money markets, and the kind of shadow banking this course studies.

To understand liquidity fully, we need to recognise that there are different prices of money. Doing so can help us appreciate what it means to have a payment system which no-one controls, because it is ultimately liquidity constraints which will define the kinds of programmable money that are useful, and the kinds that will fail.

Interest rate (future) - this is the price of money most economists focus on. It is the price of money now in terms of money later. It's how you transform money today into money tomorrow. However, there is a more primitive price which gets neglected in most thinking:

Par (now) - the price of one money in terms of another money right now. We take it for granted that demand deposits and cash reserves in a bank trade at par. In financial crises, sometimes par is broken; where private money trades at a different price to central bank money. The hybridity of our system is masked by par, but it raises the question of why does par actually work? Par is critical to the payments system - i.e. par clearing between different states (for instance) was created by the Fed. It's not easy to create this, because it is akin to a fixed price, which spooks economists. Just ask the people at MakerDAO.

Exchange rate (foreign) - the price of domestic money in terms of foreign, or world reserve, money. Which leads us to realise that there are, in fact, two dollars. This is well highlighted in the Triffin dilemma.

Price level (commodities) - economists often reference this, imagining that the quantity of money moves one-to-one with the price level of commodities.

Mehrling has a unique point of view which will assist you to uncover the actual inner workings of the "tribe of bankers" and how they think about the world so that you can program money both to account for the problems they're actually solving, and go a step further towards a more equitable world in which the bottom line is not the only thing we try to optimize.

"In this course, we will not be taking sides - pro-banker vs anti-banker - we'll be trying to figure out how the system works so that we can approach this as scientists and citizens. The world has changed: it's a global financial world. The world of 1950's textbooks is not a world with private capital markets, and it's also not global, because the global markets of the 19th Century had broken down."

Prompt: What are the four prices of money?

Interest rate, par, exchange rate, and price level.

Mehrling is trying to connect the worlds of finance and banking, so we can move towards a more holistic understanding of the overall system. His motto for doing this is simple:

"All banking is a swap of IOUs. By swap, I mean IRS, CDS and the like, but also loans. The world of finance thinks they understand everything about swaps - derivatives etc. - but we're not going to be thinking of swaps in the terms finance people do. We'll be thinking of them in the way money people do, in that there is a funding and liquidity piece to swaps and that liquidity piece is what drives all the action [...] This is all about the question, 'What does financial globalization imply for money and monetary theory'? We're trying to develop monetary theory for the real world that is around us now."

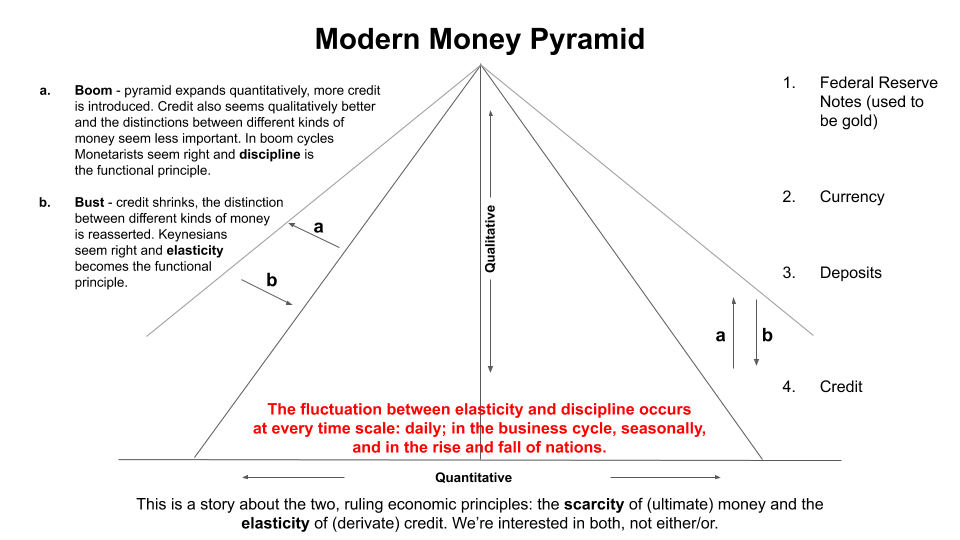

Discipline and elasticity¶

Thinking in terms of liquidity and payment systems reveals a deep tension between fiscal discipline and elasticity. Mehrling introduces the image of a pyramid, made up of different kinds of money - ranging from Federal Reserve notes at the top, to credit instruments at the base.

The critical point for our present study is that this beating heart, and the tension between elasticity and discipline, is currently managed by a group of unelected bureaucrats at the Fed. This is - to use Mehrling's phrase - neither a good nor a bad thing; it is a fact thing. They attempt to control the inevitable expansions and contractions through interest rates and various other, more contentious methods; like expanding the balance sheet and buying Residential Mortgage-Backed Securities and similar private instruments. If you're interested in why this is potentially not the optimal way to manage a global system, please read this book.

Most importantly, programmable money means that we can code our financial systems to be responsive in ways which the current system simply cannot be. We can program stability in ways previously unimaginable. But, we have to understand how hard that really is, why it is so hard, and what the trade-offs in achieving it have been throughout history. This is not about destroying central banks - Mehrling will convince you of how useful they are (preservation of par being but one example).

This is about changing the kind of money that sits on top of the pyramid from Federal Reserve notes to an ownerless, borderless, global, peer-to-peer ledger which holds us all equally accountable. It is about changing the ways in which critical financial organizations can respond to the needs of an global and interconnected system, and removing the possibility of corruption and manipulation to the greatest extent possible with the technology we have available.

Prompt: What are the two complementary economic principles we need to be able to program if we are to create a global monetary system responsive enough to replace Federal Reserve notes?

Discipline and elasticity.

Further Recommendations¶

Watch this video for more information on the deep links between money and violence - in this case the fascinating history of the Fed and the Civil War.

Watch these videos to see a worked example of balance sheet-style thinking that will explain to you how credit cards actually work (fair warning: it's a mess). This snippet will help you understand source and use accounts, and how to think about money in both micro and macro economics.

Watch this part of the course to understand how Central Banks are like clearing houses and how the entire system can be modelled effectively as one big bank.

If you've got this far, you should just watch the whole course in your own time. I learned a lot from the videos starting here - Dealers and Liquid Security Markets.

Stripe's Perspective

One of the more interesting institutional perspectives on Bitcoin as the IP layer for payments. ETH - due to its generality - already takes this a step further: you can both browse a .eth site and send payments to the same place. Though this was written in 2014, we're still fairly early in the face of all the history above.